Do IPOs still matter?

Once the ultimate milestone, the IPO is starting to look optional.

Once the ultimate milestone, the IPO is starting to look optional.

Welcome to the Alts Sunday Edition 👋

Since the 1950s, the IPO was seen as the pinnacle of success.

Going public wasn’t just a way to raise money, it signaled legitimacy. It marked a company’s arrival. A graduation ceremony. A stamp of approval in the eyes of the investing world.

But that mindset is beginning to fade. Some of the most prominent tech firms, including Stripe and SpaceX, remain private by design with apparently very little desire to ever go public.

And it’s no wonder why. When private markets are eating the world, an IPO becomes just one of many good options.

Today, we’re asking a simple but important question: In a world with more private offramps than ever, do IPOs still matter?

To find out, I spoke with four brilliant minds from the Alts community:

Let’s go

How IPOs lost their shine

Before we pontificate on the future, let’s talk about what’s happening right now.

In the 1990s, the median age of US companies when they IPO’d was 8–10 years (with a brief, sharp dip to 5–6 years during the dot-com boom)

Since then, the median has risen all the way up to 14 years in 2024.

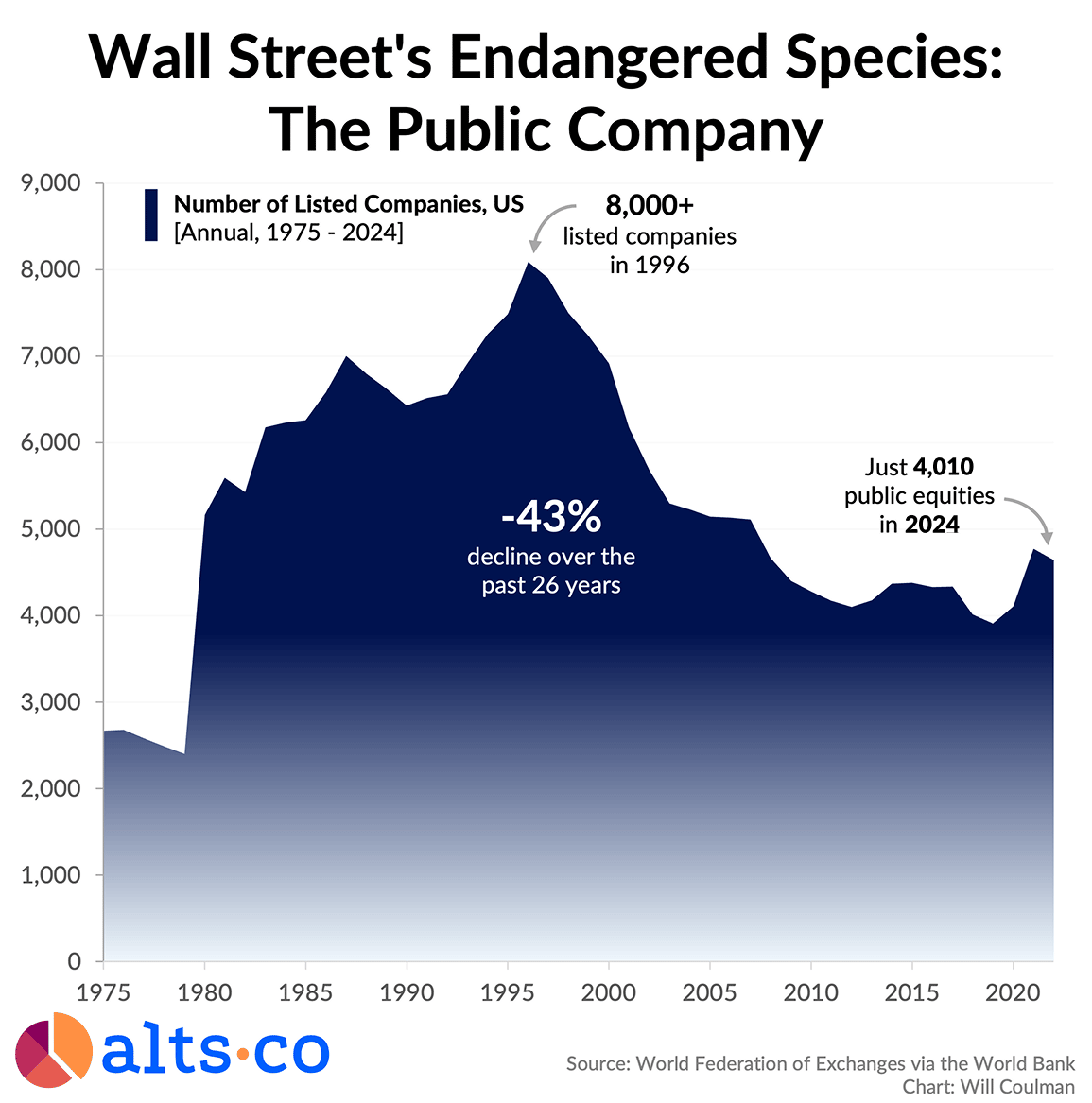

And the number of publicly traded US companies has dropped from over 8,000 in 1996 to just 4,010 today (even as the population has grown by 70 million!)

So what happened?

Two big things stand out.

Increased financial burden

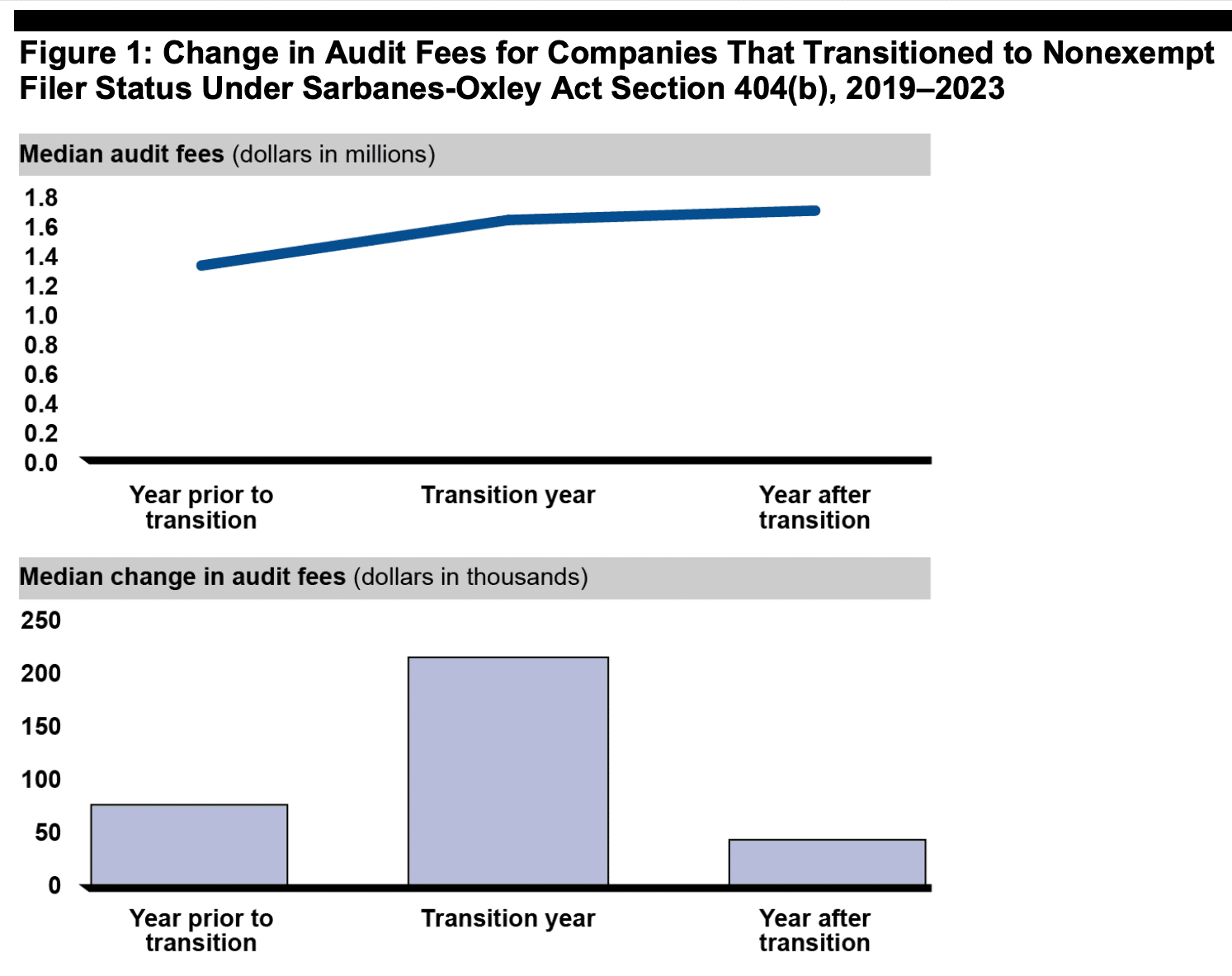

First, the sheer financial & operational burden to go public has grown heavier over time. The SEC requires public companies to report earnings quarterly — a pressure that Trump wants to eliminate.

Now you may think, “Psh, these companies can afford it!” And sure, many of them can. But for smaller companies this is absolutely a burden.

And it’s not just expensive to go public, it’s expensive to stay public. Audits and legal fees cost millions. Compliance departments have ballooned.

Chris Lustrino, CEO of KingsCrowd (a platform that tracks and analyzes the startup crowdfunding ecosystem) has watched this shift unfold in real time:

“It costs about $4 million to take a company public. You’re talking about audited financials, major accounting overhead, lawyers, bankers, investor relations, and of course the roadshow.

The thing most people don’t realize is that the cost doesn’t stop once you ring the bell — that’s just the beginning. Then you’ve got quarterly earnings to report, ongoing disclosures, Sarbanes-Oxley compliance. The administrative burden is massive.”- Chris Lustrino

Increased scrutiny

On top of the financial and operational weight, there’s also the public spotlight.

Public companies are expected to operate with a level of transparency that invites constant judgment, from investors, analysts, regulators, and the media.

And in the age of social media, boy, that spotlight is brighter than ever. Every move you make is dissected in real time. This kind of attention might be totally fine for some CEOs, but for others, it’s a nightmare.

Wyatt makes a great point:

“There’s a reason that 74 of Elon Musk’s 75 companies are private. The only one where he gets blowback or any sort of scrutiny really is Tesla.

Heck, a man can’t even approve a two trillion pay packet without it getting to the press, right? But with SpaceX, xAI, Grok — he can move money around, he can basically do whatever he wants.

Whether or not you and I think that’s great, it’s obviously preferable for him.”

- Wyatt Cavalier

But there’s also a quieter, somewhat hidden reason IPOs have lost their shine.

For years it sat beneath the surface, overlooked by many. But now it’s bubbling up fast.

The alternative private liquidity explosion

IPOs used to be the easiest way to cash out. But today, companies have more ways than ever to let shareholders sell without touching a public exchange.

As Brian Flaherty puts it:

“It used to be that IPOs were the moment when investors finally saw a return. Now, most of the action is happening before that.

There’s an entire shadow market of liquidity forming around companies that will never go public.

And it’s not just tolerated, it’s being actively enabled by everyone from the companies themselves to VC firms to regulators.”

- Brian Flaherty

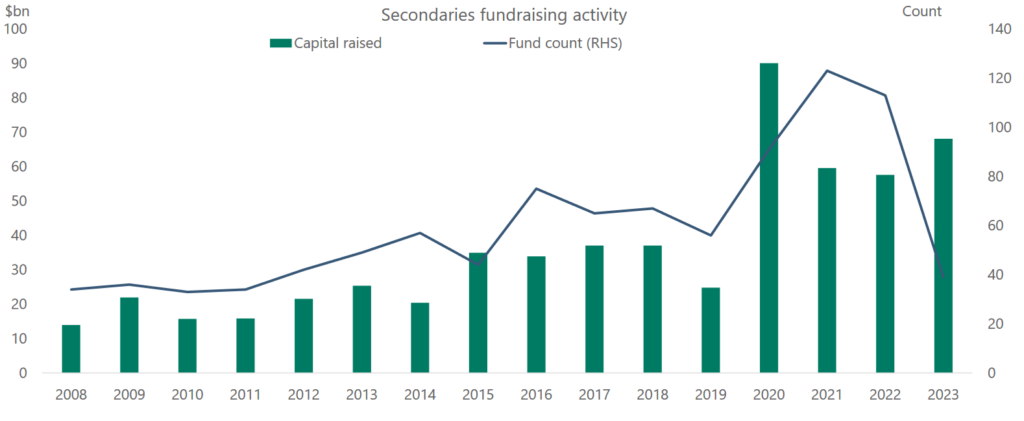

Secondary platforms, funds & brokers

Secondary platforms continue to explode. A slew of new companies are now giving retail investors access to the pre-IPO shares of privately held companies (called “secondaries.”)

Platforms like Forge, Hiive, and Nasdaq Private Market have built the rails for trading private company shares, turning them into, essentially, public markets for accredited investors.

Then there are new secondaries funds, which are popping up like AI pitch decks in a VC inbox.

The Unicorn Index Fund by OpenVC is designed to mirror the performance of late-stage startups. The ARK Venture Fund is open to non-accredited investors. So is the Cashmere Fund.

In the past, VCs were hesitant to tap secondaries markets to sell startup shares, because valuations & long-term upside can be lower than an IPO. But investor demand for hot startups (which is clearly higher than ever) often leaves them little choice.

But today, it’s increasingly orderly and transparent. Buyers have better comp data. Sellers have more choices. And brokers are stepping in to help match both sides professionally.

Christine Healey is the founder of HEALEY PRE-IPO, a concierge broker service helping people invest in individual private tech stocks.

“With IPOs being delayed longer than ever before, many institutional investors who have to manage aspects like fund life, showing realized returns to investors, rebalance their portfolios, etc have looked to secondaries as an alternative to just waiting for IPO.

The historical “taboo” around secondaries is lifting more and more, and all kinds of investors and shareholders are realizing that secondaries are a morally neutral tool that can help them achieve a variety of goals amid a backdrop of delayed IPOs and volatile public markets.”

- Christine Healey

If you feel like suddenly everyone has access to OpenAI, SpaceX, and Stripe shares, you’re not alone. At this point, it seems like the world of “exclusive pre-IPO shares” is becoming pretty commoditized.

In fact, this shift to “startup shares for everyone” has been so rapid that the companies themselves don’t know how to react. Last month, OpenAI publicly distanced itself from “unauthorized SPVs“ and Robinhood’s “stock tokens“ offering synthetic exposure to its shares.

And that’s not all Robinhood has been up to.

Robinhood’s pre-IPO fund

As we’ve been discussing in the community the big news this week is that Robinhood is launching a new publicly-traded, closed-end fund, Robinhood Ventures Fund I.

Similar to its predecessor, Destiny ($DXYZ) Robinhood’s fund will let retail investors buy into a pool of the world’s most popular startups before they go public.

(Side note: At one point, Robinhood had actually banned Destiny from its platform. Now we know why!)

We don’t yet know Robinhood’s fee structure, share count, or which startups will be included. But the filing suggests the fund will target the usual suspects: OpenAI, SpaceX, and Stripe. (God I’m getting tired of typing these same three names.)

Gerry Hayes offered some thoughts on OpenAI’s demand:

“I just don’t understand the attraction. [OpenAI] went from an undetermined valuation to a $500b valuation in just a few years. [They’re] losing billions every year, and the stock is illiquid.

Microsoft is earning tens of billions every year and the stock is liquid. And Microsoft basically owns half of OpenAI.

Why anyone would opt for OpenAI stock over Microsoft is beyond me.”

- Gerry Hayes

But in a market driven by hype and access, fundamentals may not matter as long as there’s always someone new willing to buy the bag.

Tokenization

Crypto is setting the stage for a wave of tokenized equity experiments.

The new SEC chair just came out swinging, saying “most tokens are not securities“ — a huge departure from the Gensler era.

Chris disagrees:

“From my perspective, a token is really just like a security. It enables secondary liquidity. Like it’s just a security. And if it’s a security, I don’t care if it’s on a blockchain or whatever. From what I can tell, it’s all the same.

[A buyer] is just saying, ‘I should have some form of liquidity in this.’

And that’s exactly what a Reg CF or Reg A security is.”

- Chris Lustrino

The negative part, in his view, comes from the grifter magnetism that crypto brings.

“I tend to find the people who try to do tokens are far bigger grifters than the people who just try to do a Reg A or Reg CF raise. It’s still kind of a dirty space from my perspective.

Maybe at the high end it’s not. But it’s just still a lot of shit. People just think you say ‘tokens!’ it means you’ll raise way more money.”

Brian has a nuanced view. He acknowledges crypto is messy, but he sees the rise of Reg A (mini IPOs) and Reg CF (crowdfunding) as a test run for tokenization:

“I think there are a lot of questions that still need to be answered in terms of tokenization. One is the legal question.

What does it actually mean to own these tokens that represent shares in an underlying company? Are those legally defensible claims?

Then there’s the technical question. In the crypto world there has been an astounding level of technical innovation in terms of being able to basically create exchanges and brokerages from scratch.

In the future, it seems like any company...will just be able to list their own token and invite people to participate.

And really, this is what Reg CF and Reg A have been test runs for, right? How can companies who don’t do the traditional IPO process participate in quasi-public entities?”

Winners and losers

The shift toward perpetual private status and pre-IPO liquidity may create a divide between winners and losers.

Wyatt didn’t mince words about who’s coming out ahead in this new landscape. Here’s a comment he made about Robinhood:

“I’d be interested to see who benefits from [Robinhood] the most. VCs, certainly, as they can unload shares. Founders and early employees, who will do the same. I suspect actual investors are very far down on the list.

He followed up with broader thoughts in this video:

...But the IPO fever dream that fed the investment banking-industrial complex for decades, where they get their 3% to manipulate the price of shares coming out and reward their best clients? Yeah, I think it’s coming to an end.”

Brian echoed this sentiment and took it to a 10.

In his view, IPOs increasingly happen only when all other liquidity options have failed:

“I think there’s going to be probably a lot of adverse selection in the companies that do continue to IPO.

The companies that IPO in the future are basically going to be the ones that were not attractive as a secondary offering or merger/acquisition target, and couldn’t drum up tokenization interest.

And if you’re just treating retail as exit liquidity for assets that you couldn’t sell anywhere else, I think that’s certainly a risk for retail investors. The question becomes, ‘if you had those other options, why did you IPO’?

Today, the answer to that may be rather simple: Public markets are still far larger than private ones, meaning companies can often command higher prices from a deeper pool of capital.

A well-cited paper, What Drives the Valuation Premium in IPOs versus Acquisitions?, documents that many firms going public command higher valuation multiples than comparable firms sold by acquisition — a phenomenon often called the “IPO valuation premium.”

But this paper was published in 2011, and the phenomenon may not hold true in the future!

If it doesn’t (big if) then IPOs could go from being a graduation ceremony into a salvage operation — something he already sees happening with private equity:

“They’re already trying to put PE into 401ks, which has been tabbed as one of the big “democratizations” of retail investing.

But...the more skeptical interpretation is that the private equity industry is just going to take whatever assets it can’t generate an exit out of in the traditional channels and just stuff them into 401k plans.”

- Brian Flaherty

Closing thoughts

Obviously, we’re all a bit biased here.

Alternative investing is the core of our entire business and community. If I asked four stockbrokers or RIAs the same question, “Do IPOs still matter?” I’d get four wildly different answers.

While institutional and retail capital is clearly migrating away from public markets and towards private ones, I don’t think this will happen overnight. The public company path towards irrelevance will be an evolution, not a revolution. For a few reasons.

First, while public companies may not enjoy as bright of a future as they’ve had in the past, as long as IPOs yield higher multiples than private markets, there will always be at least one good reason to go public.

But more importantly, I believe that being a public company carries not just a “halo effect”, as Wyatt put it, but a distinct weight & purpose beyond money.

I think Elon has learned the lesson from Tesla: going public isn’t worth it. I don’t think he’ll ever take SpaceX public unless he’s basically forced to.

Brian tends to agree:

“I think there will be companies so influential on society that government’s going to say, well, you don’t need to be nationalized, but you at least need to be public.

Twitter is a great example of this. Twitter was a public company and it was considered the “public square of the internet”, which gave it a stronger sense of accountability. Now that it’s private and in the hands of Musk, the idea that it’s the public square is a lot more questionable.

I can certainly see maybe OpenAI becoming so influential that a future government says, you need to be public. You need to be offering ongoing information. You need to be accountable in some sort of way.”

- Brian Flaherty

A future where publicly traded companies are those that couldn’t find an exit anywhere else (or were forced to go public by the government) seems pretty bleak.

But consider the idea that we may not even need to democratize access to those sweet private markets, because inflation might do it for us:

“There’s obviously a lot of movement right now towards expanding the accredited investor definition in the US, or even abolishing it entirely.

But [the government] is not going to update the income and net worth requirements as inflation rises! So if we take it purely at an inflationary level, eventually people’s asset values will rise to the point where pretty much everybody who seriously invests will be an accredited investor.

Even if there’s no kind of regulatory movement on accreditation, I expect most people who invest to be able to invest in private companies”

- Brian Flaherty

Hmmm... Could broad-based access to private markets simply become an inevitable byproduct of inflation?

Now that’s something to think about.

Maybe an idea for a future issue... 🤔

---

That’s it for today!

A huge thanks to Wyatt, Brian, Chris, and Christine for their help with this issue.

Find them all in the community, and bask in the glow of their sheer brilliance. 😎

See you next time,

Stefan