Groundfloor is going beyond real estate

Most investment platforms scale by going wider – more funds, more managers, and more deals.

But Groundfloor did something different. They went deeper.

The firm made a decade-long bet on durable investment architecture over quick wins. And now, that bet is starting to pay off.

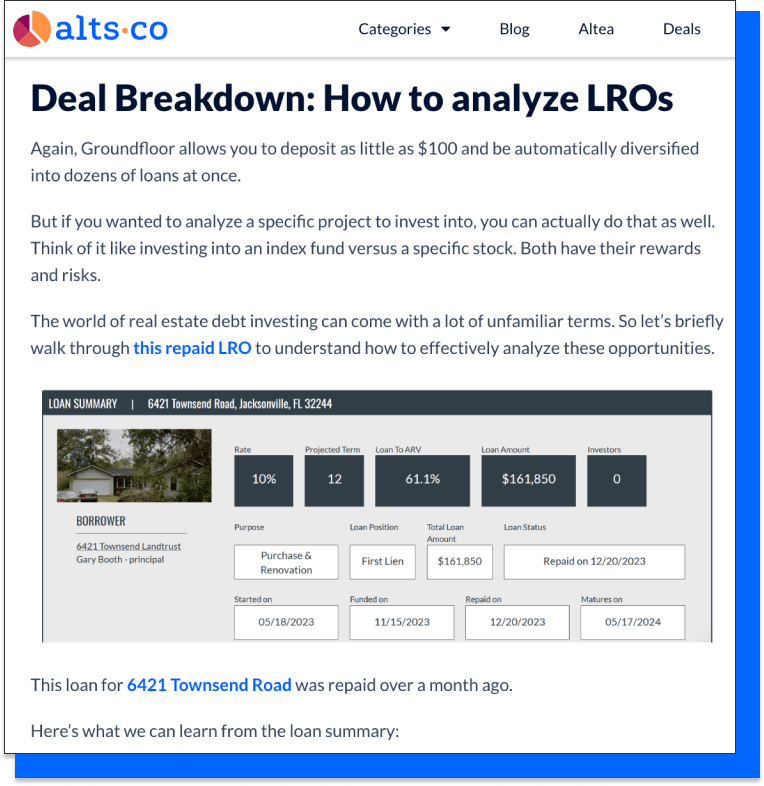

We first covered Groundfloor two years ago, focusing on the firm’s work in fractionalized real estate debt.

Today, Groundfloor is expanding beyond real estate, with options for both accredited and non-accredited investors.

With the addition of other asset classes, Groundfloor is becoming a curated gateway to private markets at large.

In this issue, we’ll explore Groundfloor’s latest offerings, and discuss:

Why most alts platforms compete on breadth – and why Groundfloor chose depth,

How Groundfloor is expanding into private credit and private equity.

Why Groundfloor partners with specialist originators in these asset classes,

And how investors can participate through Notes, Consumer Credit Portfolio II, and upcoming launches.

This issue is for readers who value investment quality over investment quantity.

Options for both accredited + non-accredited investors

Let’s go

What is Groundfloor?

Two years ago, we reviewed Groundfloor in our original deep dive on the company.

Here’s a quick reminder of what we talked about – and a bit about Groundfloor’s history:

In 2015, Groundfloor became the first company in the US to offer an SEC-qualified Regulation A security (yes, literally). Reg A broke new ground as a way for individual investors to access alternatives.

How was Groundfloor able to get started before anyone else? Simple: a deep understanding of the rules. Co-founder Nick Bhargava actually helped write the updated Reg A legislation.

At the time, Groundfloor was exclusively focused on private real estate. The company offered investments in both individual real estate loans and diversified pools of loans.

Since 2013, over 300,000 individuals have invested with Groundfloor. The company has financed over $2.2 billion in loans, with a repayment rate of 99%.

Groundfloor built this track record on real estate, and the asset class remains a core part of the firm’s operations.

But over a decade in, Groundfloor is now expanding into other asset classes – powered by the same depth and expertise that’s driven the firm’s success so far.

Going deeper, not wider

Many investment platforms scale by going downstream – they focus on adding more options at the investor level.

This isn’t necessarily wrong. But the ‘marketplace’ approach can risk sacrificing quality at the expense of volume.

Groundfloor did the opposite. Instead of scaling downstream, they’ve scaled upstream.

That means focusing on refining the inputs that drive every product on the platform – such as regulatory work, asset sourcing, and investment structuring.

Recently, I spoke with Robert Varghese, Groundfloor’s head of investments, about this approach.

Here’s how Robert put it:

“The goal for us is not to become a marketplace – we’re not terribly interested in that. What we think is important is finding pockets within private markets that are relatively unique, innovative, and differentiated, and structuring them in a favorable and accessible way for our clients.”

Here’s what that upstream focus looks like in practice:

Building fund architecture expertise – so that individual investors can participate at low minimums.

Mastering SEC qualification – so that new investments can be offered with lower fees and less friction.

And partnering with specialist originators – so that retail investors get access to institutional-grade opportunities.

If that sounds dense and complex, it’s because it is.

Groundfloor spent a decade building this infrastructure. They’ve proved that it works in private real estate.

Now, they’re putting it to work everywhere else, with the aim of becoming the front door for investors looking to build a diversified private markets portfolio.

Let’s look at Groundfloor’s offerings.

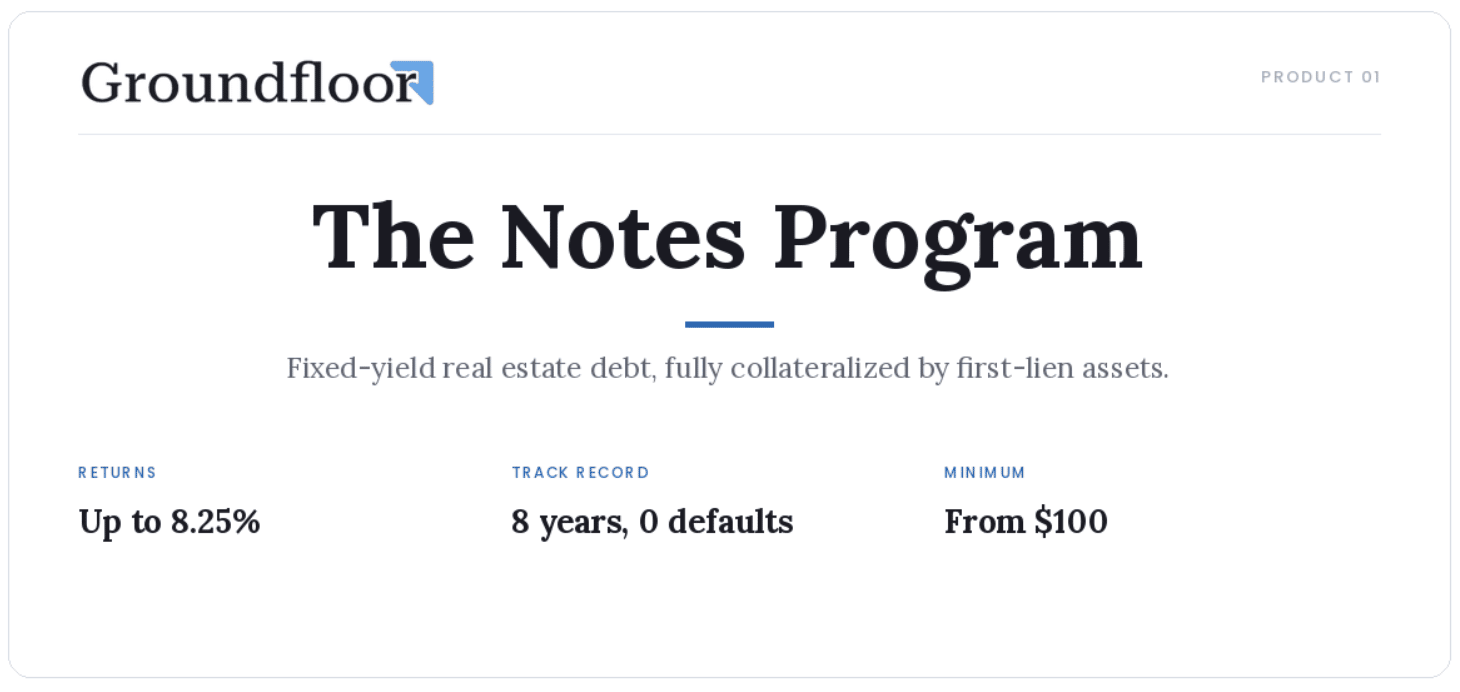

Product #1: Groundfloor Notes

We covered Groundfloor’s real estate Notes in our original deep dive.

But it’s worth revisiting in depth, since Notes have changed substantially since we first covered them.

They’ve become an ideal gateway for investors new to Groundfloor.

Groundfloor’s Notes are essentially pooled investments in real estate loans. Investors provide capital that Groundfloor deploys across its underlying loan book.

In other words, Notes are fully collateralized by real estate assets -- but offer a fixed yield rather than tying returns to any single loan.

Over the past eight years, the program has built up a strong record of delivering for investors. Groundfloor has not reported a single late, missed, or defaulted payment.

Previously, Notes had a wide variety of terms, rates, and structures. But last year, Groundfloor decided to simplify everything down to three products:

A 1-month note at 4.75% fixed return, with deferred interest and a $100 minimum.

A 3-month note at 5.75% fixed return, with quarterly returns and a $100 minimum.

And a 12-month signature note at 8.25% fixed return, with monthly interest and a $1,000 minimum. (This is Groundfloor’s most popular Note thanks to its high monthly fixed yield.)

All of Groundfloor’s Notes are available to both accredited and non-accredited investors. Each note rolls over automatically at maturity unless investors specify otherwise.

These changes might seem small. But the impact on the Notes program has been big – assets under management have grown by nearly 40% since rolling out this standardized structure.

The 1-month note: Take Groundfloor for a test drive

Of these three notes, the 1-month is unique. After all, why offer such a short-duration product in the first place?

When I asked Robert about it, his answer was clear: building investor trust.

“The 1-month note is the shortest-duration instrument on our platform. But that’s exactly the point – in one month, investors get to see if we can deliver. Once we’ve earned trust through actual results, they can move on to explore our other offerings.”

Many platforms ask investors to lock up capital for years on the strength of marketing or historical returns.

But through the 1-month note, Groundfloor offers a low-stakes way for investors to see for themselves whether the firm can actually deliver.

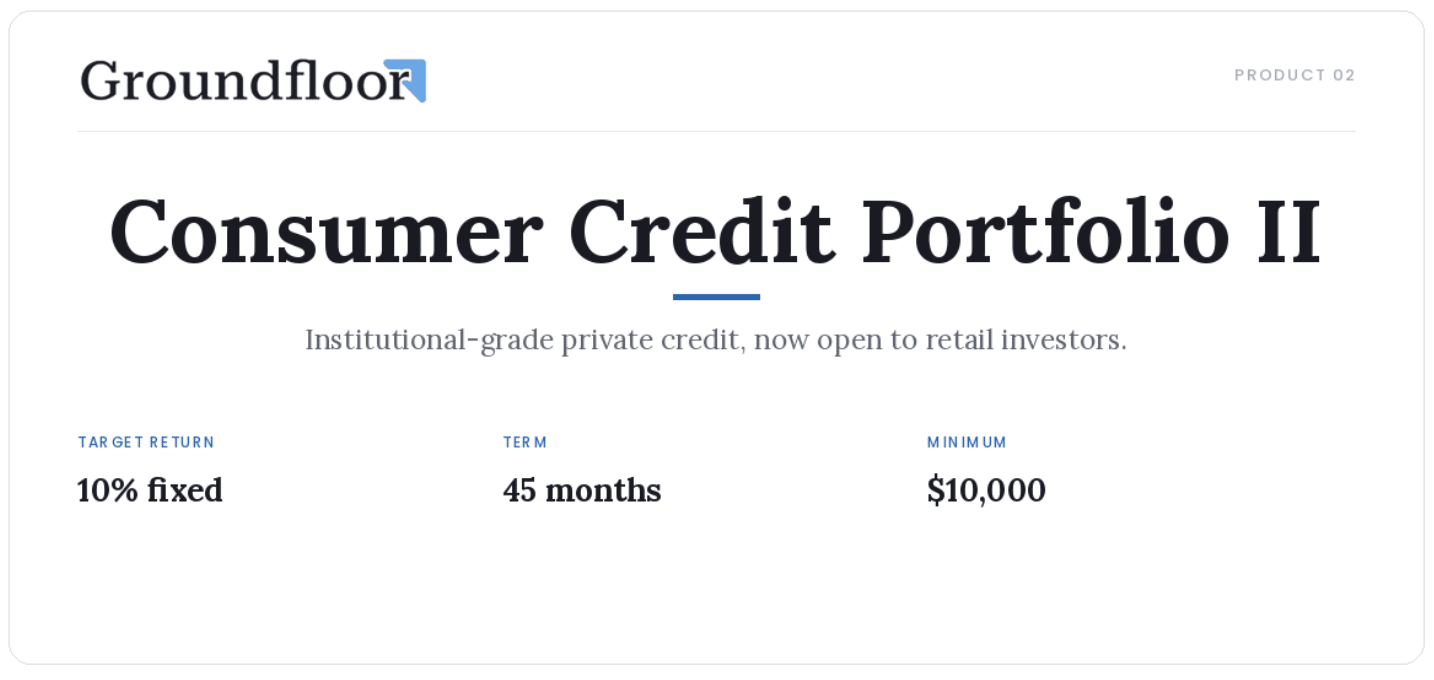

Product #2: Consumer Credit Portfolio II

The Notes program proves that Groundfloor’s infrastructure works in real estate. But what about beyond it?

Earlier this year, Groundfloor launched its first investment product outside real estate: a private credit fund focused on short-term consumer loans.

The results were immediate. The initial $1M offering was 40% filled within 48 hours – and ultimately oversubscribed.

Now, Groundfloor is back with the next iteration – Consumer Credit Portfolio II.

The market opportunity: Consumer credit as a diversifier

Private credit has historically focused on direct lending to businesses. But lending to consumers offers some distinct benefits:

The market is massive. US consumer credit outstanding currently exceeds $5 trillion, providing ample opportunity for specialist underwriters.

Demand for short-term consumer loans has historically been resilient in periods of economic stress, when traditional markets can struggle.

Most importantly, this is an asset class that’s traditionally been institution-only. There are very few funds or platforms that offer individual investors access to consumer lending.

That last point is exactly the kind of gap Groundfloor’s upstream model is designed to address.

Specialist origination: Hive Financial Assets

When it comes to asset origination, Groundfloor’s expertise is in real estate loans.

That’s why the firm has partnered with Hive Financial Assets for its consumer credit offerings. Hive is a specialist private credit manager that’s developed a strong track record since launching in 2017:

Hive has already scaled to over $160M in assets under management.

The firm focuses on short-term loans (~9 months), keeping the portfolio relatively liquid.

Hive reports an average quarterly return of ~3.6% on the underlying loan book (~14% annualized).

Hive handles origination, underwriting, and ongoing loan management. Groundfloor handles structuring, SEC qualification, and retail access.

Full details for Consumer Credit Portfolio II:

Target return: 10% fixed annual

Fees: None

Distribution schedule: Quarterly

Term: 45 months (36-month core + 9-month runoff)

Minimum investment: $10,000

Total offering: $3M

Investor restrictions: Accredited only

The offering window is tight – the deal opens May 4 and runs through May 24, or until fully subscribed.

Given that the first iteration filled before reaching its cap, interested investors should consider acting quickly.

Express Interest in Consumer Credit →

Open until May 24

Coming Soon: Two New Verticals

Notes and Consumer Credit Portfolio II are live offerings investors can act on today.

But Groundfloor continues to expand. The firm is preparing to launch two additional products in the coming weeks – each with a specialist originator and the same upstream infrastructure.

Homegrown: Financing local businesses

The first upcoming launch is a small business financing partnership with Homegrown, an Atlanta-based fintech.

Homegrown focuses on a niche segment: brick-and-mortar small businesses (think local restaurants and hair salons) that already have one or two locations and are looking to expand.

This kind of business often has limited financing options:

SBA loans can be a lengthy and bureaucratic process,

Merchant cash advances often come with onerous terms,

And traditional banks frequently require personal guarantees that put personal assets at risk.

Homegrown occupies a distinct niche, offering flexible, cash-flow-based financing without personal guarantees.

Repayments scale with monthly business revenue, aligning Homegrown’s interests with the success of the business.

This partnership is particularly meaningful for Groundfloor. Both firms are Atlanta-based, which means the company is helping fund the kind of local businesses that anchor its own neighborhood (and possibly yours, too).

Groundfloor expects to launch the Homegrown offering in late May.

Express Interest in SMB Financing →

Serengeti: Pre-IPO single-stock financing

The second upcoming launch is a private equity fund in partnership with Serengeti, a firm specializing in pre-IPO single-stock financing.

Here’s a brief overview of pre-IPO financing and how Serengeti’s model works:

Employees at top private companies face a liquidity problem. They often hold significant equity, but usually can’t access cash from those holdings until the company actually goes public.

Serengeti bridges that gap. The firm provides employees with liquidity today, using their pre-IPO shares as collateral. When the company eventually exits, Serengeti participates in the upside.

The fund will target a curated portfolio of approximately 25 category-leading, late-stage private companies with public-ready financials and a near-term path to liquidity – names that, in the institutional channel, typically require $1M+ minimums. Through Groundfloor, investors will be able to participate at much lower entry points.

This opportunity will only be available to accredited investors.

This is a meaningful expansion for Groundfloor – the firm’s first foray into private equity.

Express Interest in Pre-IPO Financing →

Why Groundfloor’s approach matters right now

So far, we’ve focused on Groundfloor itself. But it’s worth zooming out for a moment.

The past few months have been a difficult stretch for several areas of private market investing. Multiple high-profile private equity and private credit funds have stumbled, with concerns over frozen redemptions and valuation transparency.

I asked Robert what he thought about the current state of the market. Here’s how he put it:

“I think a lot of the issues you’re hearing about in private credit today have to do with a mismatch – a mismatch of the actual thing you’re investing in, the wrapper that it was put in, and the expectations given to the end investor.”

That last point – investor expectations – is arguably the most important one.

Many private credit funds were built for institutional investors, who are aware of what they’re getting into. As Robert explained, the challenge is when firms then try to repackage these products for retail audiences – often with imperfect wrappers and unclear communication.

Groundfloor’s approach to this challenge is straightforward: get the wrapper right and tell investors the truth about what they’re buying.

In practice, that looks like:

Matching duration to product. Short-term capital goes into short-term notes. Longer-duration capital goes into longer-duration vehicles. After all, a 12-month investment shouldn’t pretend to have daily liquidity.

Clear communication on tradeoffs. Liquidity is one of the first things that Groundfloor’s investment team raises with new investors. If immediate access to funds is the top priority, private markets aren’t always the right fit.

Education over hype. Groundfloor has consistently chosen to onboard investors gradually rather than push them into the highest-yielding product on day one. This helps ensure that investors truly understand – and are comfortable with – their holdings on the platform.

The bottom line: Groundfloor builds investments that match what investors actually need – not necessarily what’s easiest to sell.

And in the current environment, that’s never been more important.

Where to start with Groundfloor

If you’re interested in Groundfloor, where should you actually get started?

That depends on what you’re looking for:

If you want passive income from a single Groundfloor product, the 12-Month Signature Note at 8.25% is the obvious place to start. Monthly distributions, fully collateralized by real estate, $1,000 minimum, no fees – and it’s available to all investors (no accreditation required). For investors who want a shorter horizon first, the 1-Month (4.75%) and 3-Month (5.75%) Notes are available at a $100 minimum.

If you’re sold on Groundfloor and want to diversify, Consumer Credit Portfolio II is the deal to focus on right now. The offering is designed for investors who want consistent income from a less-correlated corner of private credit, with a 10% target return and no fees.

If you’re interested in more differentiated strategies, Serengeti and Homegrown are worth keeping on your radar. Pre-IPO single-stock financing and small business expansion financing are typically gated to investors with $250K+ minimums. Through Groundfloor, you’ll be able to access them at a fraction of that.

Aside from the opportunities already mentioned, another way in which investors can invest with Groundfloor is through the company’s upcoming Convertible Debt Note offering.

This is a chance to earn 11.5% annually (paid monthly) and acquire Groundfloor’s stock at a discounted rate.

Groundfloor believes that as the company grows, its client base should have the opportunity to grow right along with it.

The next opportunity to purchase Groundfloor stock is expected to take place over the summer, likely in June or July.

That’s it for today.

As always you can find me in Altea Community.

Until next time

Brian

Disclosures

This issue was written by Brian Flaherty, and edited by Stefan von Imhof

The Groundfloor team was able to review an early draft of this article. Brian and Stefan made final editorial decisions.

Alt Assets, Inc has no holdings in Groundfloor or any companies mentioned in this issue

Stefan is considering investing in the Consumer Credit Portfolio II fund.

Disclaimer from Alts

This issue is a sponsored deep dive, meaning Alts has been paid to write an independent analysis of Groundfloor. Groundfloor has agreed to offer a deep look at its business, offerings, and operations. Groundfloor is also a sponsor of Alts, but our research is neutral and unbiased. This should not be considered financial, legal, tax, or investment advice, but rather an independent analysis to help readers make their own investment decisions. All opinions expressed here are ours, and ours alone. We hope you find it informative and fair.