Let's go to China

Welcome to the WC.

This summer, I’m planning to take my family to China for eight to ten weeks. The aim, beyond showing my wife and kids a good time, is to get a feel for the country from an investor’s perspective.

The default view of China, I think, is that there’s an incredible opportunity there, but it’s very difficult for a foreigner to understand, let alone access.

Am I right?

As part of my preparation for the visit, I’m going to sort of open-source my desktop research through June. Where my head’s at, what I’m exploring, and where the opportunities may be (and where they aren’t).

Today, we start out broad.

💻 What can you invest in with just a laptop

💪🏽 What’s available with some effort

⛔ What’s totally off the table

Let’s go 🚀

Let’s kick it off from the top.

Why spend an entire summer in China? Why would anyone want to invest there? It’s far away and feels very hard as a foreigner.

Why go through all the trouble?

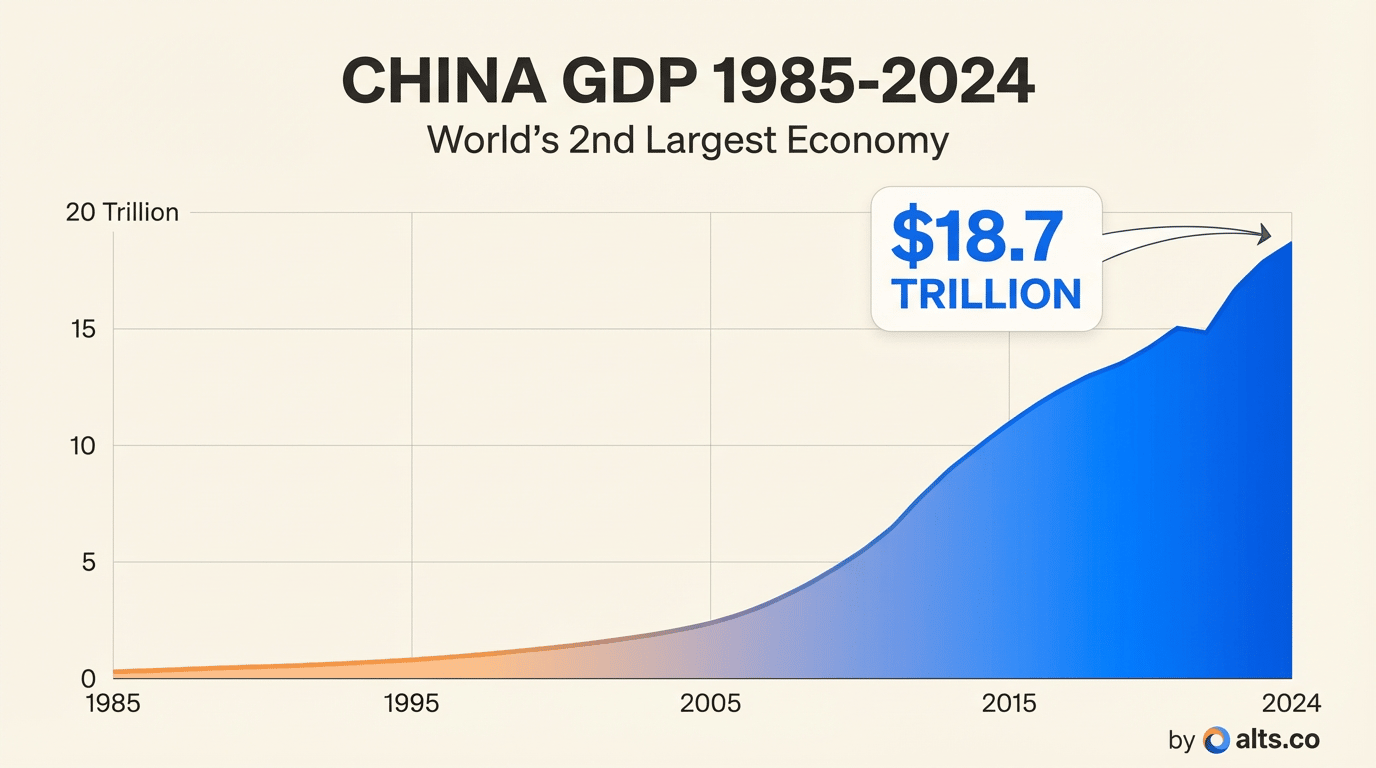

Because it’s a $20 trillion economy growing at 5% a year, and the vast majority of the global population thinks it’s untouchable.

Demand is artificially low, which means valuations are, theoretically, correspondingly depressed as well.

China’s GDP hit 140 trillion yuan in 2025.

Three individual Chinese provinces each produce more GDP than Saudi Arabia.

Its manufacturing output exceeds the next nine largest manufacturing nations combined.

Its stock market crossed 100 trillion yuan in market capitalization for the first time ever last August.

There are over 1,000 billionaires.

142 of the Fortune Global 500 are headquartered there.

And yet.

Most Western investors, particularly in the alternative space, treat China like it doesn’t exist. They’ll happily wire money to a bourbon distillery in Kentucky, a startup in Silicon Valley, or a fractional racehorse in Florida. But the world’s largest manufacturing superpower? Too hard. Too risky. Too far away. Too opaque.

I get it. It is complicated. Capital controls are real. The legal system works differently. The regulatory environment moves fast, and not always in the direction you’d like.

For a foreign retail investor, the simple act of opening a brokerage account is essentially impossible unless you live there.

But “complicated” isn’t the same thing as “impossible,” and the gap between those two words is where the returns live.

Hard-to-access markets reward people who do the work. That’s literally the entire thesis behind alternative investing. If everyone could do it, it wouldn’t pay.

So this summer, I’m going to find out how hard it actually is on the ground, with my family, for eight to ten weeks.

Let’s begin by mapping access.

What’s easy as a foreigner? What takes real effort? And what’s completely off the table?

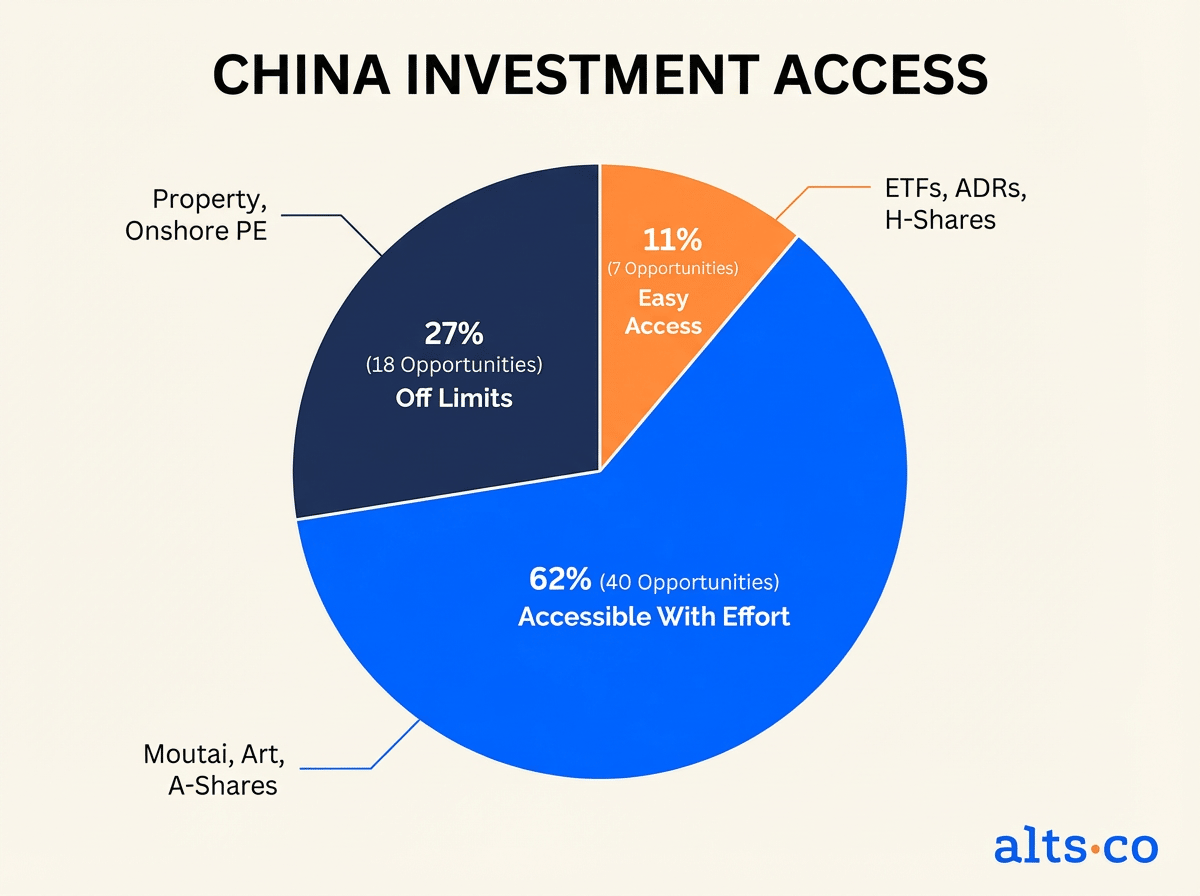

I spent the last couple of weeks mapping every investment opportunity I could find that a foreigner might conceivably access in China. Not just public markets. Everything. Physical goods, sourcing, import/export, alternative assets, private markets.

I ended up with 65 distinct opportunities in three buckets:

Easy Access: 7

Do these from your laptop. No travel, no relationships, no special licence.

Accessible With Effort: 40

Requires physical presence, supplier relationships, a Hong Kong brokerage, accredited investor status, or local knowledge.

Off Limits: 18

Closed to foreign individuals, effectively dead, or structurally impossible.

The easy stuff requires no travel. The middle 40 is where the trip creates genuine edge. The 18 are time sucks to know about, so you don’t run into them.

I’ve put together a full matrix with all 65.

💻 What can you invest in with just a laptop

Seven things.

Six financial products and one research opportunity:

H-Shares are Chinese companies listed in Hong Kong, often trading at 20-40% below the same company’s A-share price on the mainland. The spread is a structural arbitrage caused by capital controls.

ADRs give you Alibaba, JD, and PDD on US exchanges. But you own a depositary receipt, not the share. The VIE structure underneath means you may not legally own the underlying Chinese entity.

China-focused ETFs (FXI, KWEB, MCHI, ASHR) are the easiest entry point. They all hold different stuff, which is worth understanding before you buy.

Dim Sum Bonds offer offshore RMB exposure.

Shanghai Futures on iron ore, crude, and copper are open to foreigners. Interesting fact: real price discovery for iron ore now happens in Shanghai, not London. Most Western investors don’t know that.

And the entire WeChat/Alipay ecosystem. These are mandatory on the ground, and I suspect every transaction during the trip will be a research session.

If you’re reading this newsletter, you probably want more than index funds, so let’s get off the sofa and dig into the meat of things.

My view on investing in China

I’m already investing in China

I’d like to invest in China but don’t know enough

I’m not interested in investing in China

💪🏽 What’s available with some effort

Forty opportunities.

For your sanity’s sake, I’ll group these rather than walk through each one. The full matrix, which I’ll share in the Altea community, will have the details.

Public markets with extra setup.

A-Shares via Stock Connect (~5,000 domestic stocks, need HK broker).

Chinese government and corporate bonds via Bond Connect.

C-REITs (infrastructure REITs launched in 2021, but it’s fairly immature, with only around 30 listings).

Corporate bonds are genuinely interesting because the market is huge and almost entirely opaque. Rating agencies are unreliable, and SOE guarantees are unwinding.

Private markets.

Distressed debt (post-Evergrande, there’s $300bn+ in property developer distressed debt with recovery rates of 5-30%).

Offshore real estate funds (hammered from 2022-2024, but 2025-2026 vintages could be interesting).

I’d love to hear from anyone in the community who’s deployed capital in these.

Export from China.

This is where I start to get excited. Some headlines:

White-label consumer goods (40-70% gross margins).

Electronics sourcing from Huaqiangbei (markups of 200-1000% vs Western distributors, but billions in counterfeit chips).

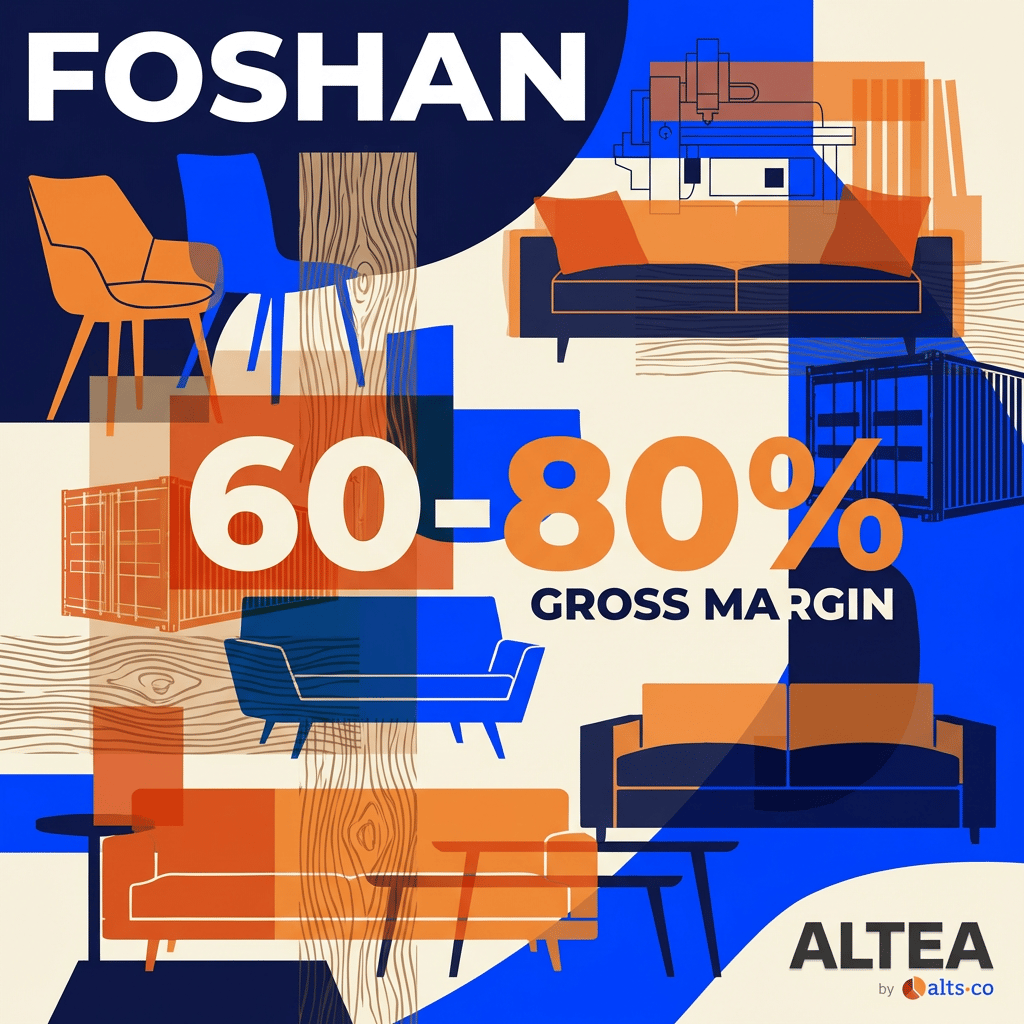

Furniture from Foshan (60-80% gross, the world’s largest furniture market).

OEM product development (a full product development cycle can be done for under $10K in Shenzhen).

This doesn’t even touch robots, drones, and electric vehicles that crush Western competition.

Import into China.

The reverse flow.

Spanish premium food commands 2-5x the European retail price in China, and since I live in Spain, this might be the most personally aligned opportunity.

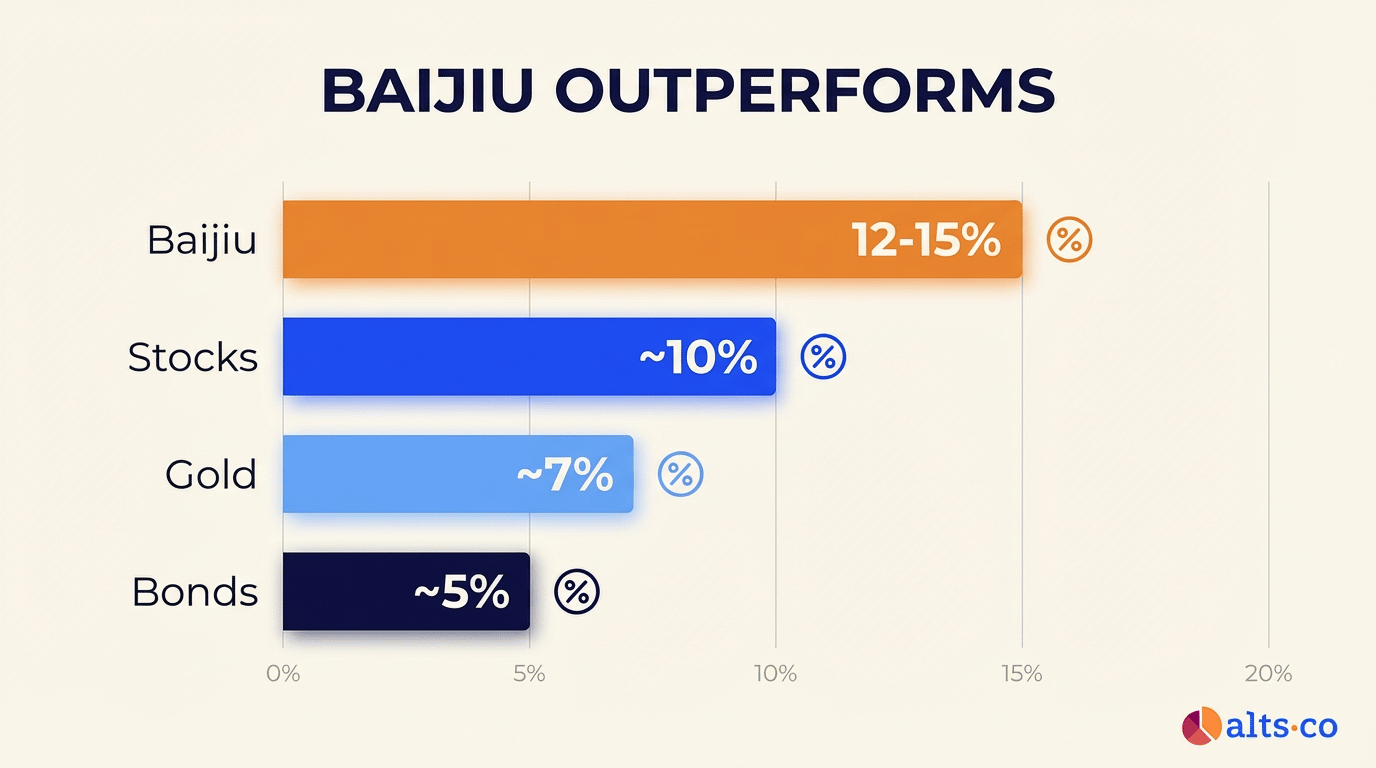

Premium tequila is growing by 60%+ per year in China, and we have an excellent source of it. Early research suggests margins of up to 80%.

Infant formula still faces enormous demand from foreign brands because the 2008 melamine scandal permanently destroyed domestic trust.

Pet food is a $40bn market growing 20%+ annually.

Educational toys absorbed spend after the $100bn+ tutoring ban.

And daigou personal shopping networks remain a $50bn grey market despite a 2019 crackdown.

Physical goods as assets.

Now we’re in proper WC territory.

Moutai’s 10-year CAGR has beaten the S&P, but ~70% of the vintage secondary market is fake.

Aged pu-erh tea appreciates 10-20% annually for good vintages (similar to whisky cask investing).

Chinese contemporary art is the world’s #2 market, and post-crackdown luxury spending has shifted into it. Beijing 798 and Shenzhen OCT Loft are both on the itinerary.

Sourcing and operations.

This is how many expats actually make money in China.

There are a variety of on-the-ground services, such as sourcing agent commissions, QC inspection services, and factory relationships, that help buyers secure 10-30% better pricing than on Alibaba.

Their networks comprise WeChat groups with factory owners rather than Alibaba search results, are the real edge.

Everything here could be worth looking at, and that’s probably going to be my main focus in the months to come. I’ll dig into all these a bit and dive deep into maybe a half dozen before wheels up in June.

⛔ What’s totally off the table

Eighteen things you can’t do or shouldn’t bother trying.

Closed to foreign individuals.

Onshore PE funds (institutional only).

Direct lending (courts don’t prioritise protecting foreign creditors).

LGFV bonds ($9 trillion+ outstanding). This is THE systemic risk in China, and nobody outside the country analyses this properly.

Residential property (you can buy one unit after one year of residency, and you never own the land, because all Chinese property is leasehold).

Onshore distressed-asset auctions (hahahahahaha, good luck).

Effectively dead.

P2P lending (5,000 platforms shut, $150bn gone, largest sector destruction by regulatory decree in modern history).

Dropshipping (courses about it are more profitable than doing it).

Structural gaps.

This is the part I found most interesting. These are investment vehicles that literally don’t exist in China, and each gap reveals a structural issue.

There are no tax-advantaged retirement accounts. No 401(k) or ISA equivalent. This partially explains Chinese retail investor behaviour: all that savings goes into property and A-shares because there’s no tax-efficient wrapper pushing people toward index funds.

No farmland or timber REITs. These can’t exist, because all land is state-owned. You can’t securitise ownership of something that doesn’t exist.

No tax liens or tax deeds, because there’s no mature property tax system. When property tax arrives, this could change. It’s the biggest pending structural change in China’s fiscal architecture.

Finally: No music or content royalty markets, no equity crowdfunding, no SPACs, no revenue-based financing, no Opportunity Zones.

I find the gaps more revealing than the opportunities in some ways. They’re a map of what’s structurally different about the economy. If you don’t understand them, you’ll make assumptions that don’t apply.

So what have we got?

Seven ideas you can do from your sofa, 40 that require effort, and 18 that are off limits.

Over the next few months, I’ll dig into specific sectors from the middle tier to figure out where the on-the-ground alpha is. Fingers crossed for tequila.

If you have experience investing in or doing business with China, I want to hear from you. Hit reply or post in the Altea community. I’m building this in public because I think our community knows more collectively than I do individually.

Let’s make the most of it.

That’s all for this week; I hope you enjoyed it.

Cheers,

Wyatt

© 2025 Alt Assets, Inc.

651 North Broad Street, Suite 206 Middletown DE 19709

Join the Alts Community | LinkedIn | YouTube