Let’s make a sequel

Welcome to the WC, where you’re trapped in my mind for eight to twelve minutes weekly.

Last week, we bought a trip aboard the Tequila Express to see how the Jalisco tourism market compares to Kentucky’s Bourbon trails.

The analysis supports our potential investment in Tequila III; the memo is coming out soon (manana manana).

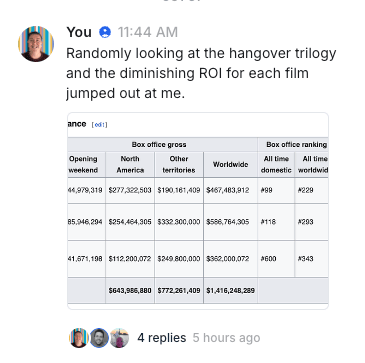

This week, I went down the film sequels rabbit hole after spotting and posting this in the Altea community.

So obviously, I spent 15 hours conducting AI-assisted linear regression analysis to figure out:

What determines a sequel’s success, and

Of upcoming sequels/follow-on films, which will succeed?

I’ve built a fairly robust model for this that may come in handy for our Launch JV endeavour.

Let’s get to it.

When it comes to box office hits, sequels and franchises are where it’s the money’s at.

How many films above were not part of a larger franchise or a sequel when they were made?

Minecraft

Barbie

Finding Nemo

Maaaaybe Guardians of the Galaxy

Avatar

Fully 92% of the 21st century’s top grossing films were the second, third, tenth or whatever film in a series or franchise.

The only two holdouts:

Barbie, and there’s an easy argument there that the film was part of a franchise with prior cartoons etc.

Avatar, which of course became a franchise and had David Cameron, who directed three of the top four grossing films ever.

All of which is to say sequels and franchises are important to the film industry and therefore interesting to me.

And the nice thing about sequels and such is that there’s a lot of data you can use to figure out what’s going to work and what’s not.

This week, I dug into 165 films over 45 franchises from 2000 to 2025, analysed nearly a dozen variables, and built a model that tells me (hopefully correctly) what works and what doesn’t.

So what did I learn?

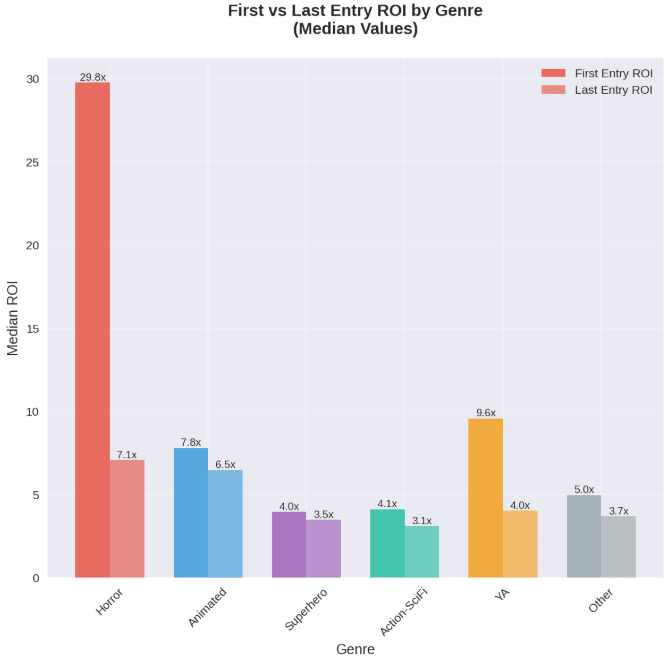

3️⃣ The rule of three

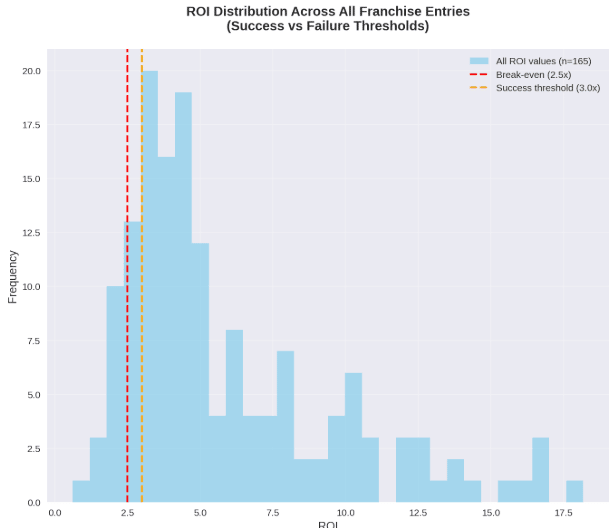

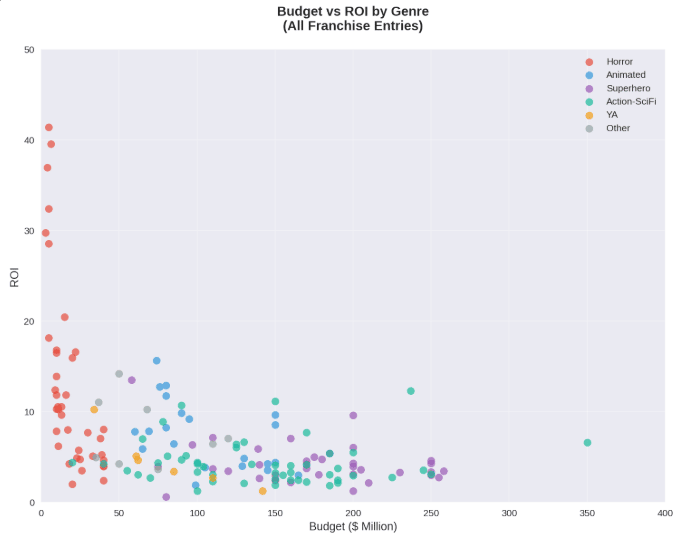

In film, ROI isn’t “profit.” It’s simply worldwide box office divided by production budget. The problem is everything that sits between revenue and cash: marketing (tens of millions) and exhibitor splits (cinemas keep a big chunk).

In practice, a movie needs roughly 2.5–3.0× its budget at the global box office just to break even on cash. Treat 3× like your hurdle rate. If a sequel costs $120m, a $300m forecast is not exciting—it’s par. You want a credible path to $360–480m so the upside pays for slippage elsewhere in the slate.

And beware of the classic value trap: after a soft entry, spending more rarely fixes demand. Bigger set pieces raise the break-even faster than they raise intent. The correct play is to right-size costs to the audience you actually have, not the audience you wish you had.

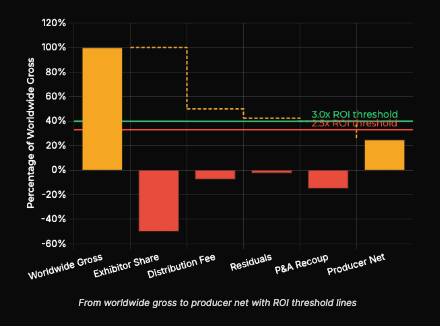

Where does all the money go?

First, marketing typically runs 50–100% of production cost for major releases. Low-budget horror often spends triple its production budget on advertising. Second, theaters keep roughly 50–55% of box office revenue. Studios see about half of every ticket sold, less overseas.

Is horror as great as everyone says?

We’ve gushed repeatedly about the ROIs you can acheive investing in horror films.

And it’s true. But it’s also not as simple as that.

First, there’s a lot of survivorship bias going on here. Hundreds of low-budget horror films go nowhere and are watched by no one but the director’s mum. Those don’t get factored into the champagne stories because no one hears about them.

Second, original horror behaves like early-stage startups: low checks, high variance. Once you land a hit—a memorable creature, hook, or villain—the sequel math flips in your favor.

Budget stays lean ($5–20m), awareness is built-in, and opening-weekend cash arrives before word-of-mouth cools. That’s why horror sequels routinely print 5–10× ROI even when reviews are “fine, not great.”

Terrifier 3 cost $3 million to produce and grossed roughly $80 million at the box office—a staggering ~27× ROI. Throw in a marketing spend of just $500k, and you’re looking at the most profitable film of 2024 by pure return on investment. Not bad for a slasher about a homicidal clown.

Two rules keep the cash machine humming.

First, don’t overcapitalize the follow-up. If the first worked at $12m, resist the urge to spend $40m; you’re selling a jolt, not a city-destroyer.

Second, fresh edge, same promise: change location, deepen the lore, raise one signature set-piece—without muddling what the audience came for.

The moment horror sequels balloon past $60–70m, they start playing by blockbuster rules. A Quiet Place: Day One had a $67m budget and earned $260m worldwide—solid, but nowhere near horror-tier multiples. The magic zone is $5–20m budgets where a modest hit generates outsized returns.

Think of original horror as an option and sequels as harvest mode.

As an investor, you want to find a producer making a second film after a breakout smash horror hit.

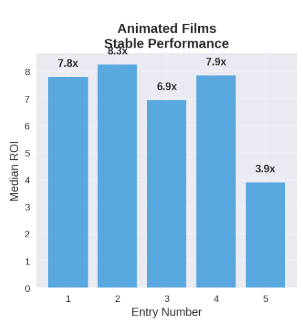

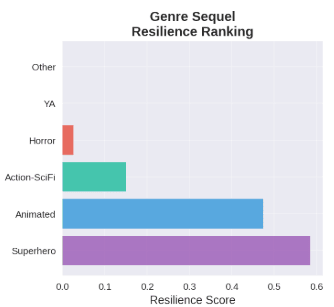

Family animation is a compounding machine

Family animation behaves like a durable consumer brand. Kids age in every cycle, parents repeat-buy, and the films travel globally with excellent dubbing. Budgets are can hit nine figures, but when story quality holds, you repeatedly see 4–7× ROI across several films with less volatility than live action spots.

The numbers bear this out.

Inside Out 2 had a $200m budget and pulled in $1.7 billion at the global box office—an 8.5× multiple and roughly $650m in net profit. It’s now the most profitable animated film ever and the most profitable film of 2024, period.

Despicable Me 4 delivered a 9.7× multiple on a lean $100m budget. Kung Fu Panda 4 hit 6.4× on just $85m.

The flywheel works like this:

school holidays create natural demand spikes

week-to-week drops are gentle, and

ancillaries (toys, music, streaming, parks) lengthen the tail.

Star Wars generates $3 billion per year in toy revenue; far more than most of its films earn theatrically.

What breaks the machine?

Story staleness (“last time, but louder”) and cost drift (set-pieces and salaries creep up, silently lifting break-even). Disney’s upcoming Snow White reportedly ballooned to a $270m budget. A nightmare no prince can wake you from.

Compare that to Illumination’s relentless discipline: they consistently deliver films in the $80–100m range while Disney and Pixar skew $150–200m or higher.

The winning play is boring but effective: control costs, add a genuinely new character/locale/emotional beat each time, and release into family-friendly timeframes.

YA almost always bombs today

YA (young-adult novel adaptations) once ruled Friday nights, but most struggle today.

There are lots of reasons for this that are pretty obvious when you take a step back.

Aging out: a two-year gap turns a 16-year-old superfan into an 18-year-old with new habits. The characters and story stay the same while the audience gets older.

Serial risk: if Film 1 is merely “fine,” Film 2 feels like homework—you’re asking casuals to re-engage with lore they didn’t love.

Limited four-quadrant pull: parents, younger kids, and older adults don’t care about werewolf vampire human love triangles, so you miss the “bring everyone” multiplier that powers animation and superheroes.

Attention competition: TikTok, gaming, and creators ate the teen time budget; if your film isn’t a social moment, it disappears.

Over-budgeting: glossy YA sequels assume a huge international market that often isn’t there.

The big exceptions (Hunger Games, Twilight) were true cultural events—and they ended while the audience still cared. Meanwhile, the Divergent series collapsed mid-franchise with its final film never released theatrically. Maze Runner saw diminishing returns with each entry. Most 2020s YA adaptations either went straight to streaming or were DOA (which is, incidentally, a great film).

Harry Potter notably avoided the aging out issue above by ensuring the characters grew and themes became more mature.

🇨🇳 The China problem

Then there’s the 800lb dragon in the room: China is no longer reliable.

From 2012–2019, Hollywood could bank on Chinese box office to bail out underperforming sequels.

Transformers: Age of Extinction (the fourth film) grossed more in China ($320m) than in the U.S. ($245m)

Warcraft bombed domestically but pulled $220m in China, turning a disaster into a marginal success

Fast & Furious sequels became progressively more China-dependent, with Furious 7 pulling $391m from China alone

Pacific Rim flopped in the U.S. ($102m) but made $112m in China, greenlighting a sequel based purely on Chinese appetite

This created a dangerous feedback loop: studios would greenlight sequels with weaker domestic prospects because China offered a safety net. The franchise could be declining in America, but as long as Beijing loved explosions and CGI spectacle, the math worked.

Those days are over. Chinese regulators limit Hollywood releases, domestic Chinese films now dominate the market, and cultural/political sensitivities make certain genres and themes non-starters.

A couple case studies 👇

Marvel

Avengers: Endgame (2019): $629m China box office

Doctor Strange 2 (2022): $0 China box office (never released)

Ant-Man 3 (2023): $0 China box office (never released)

The Marvels (2023): $0 China box office (never released)

Marvel spent a decade training Chinese audiences to see every sequel as a cultural event. Then regulators pulled the plug, and suddenly films budgeted assuming $100–200m Chinese contributions had to survive without them.

Fast & Furious

Fast Five through Furious 7 (2011-2015): averaged $250m+ in China

Fast X (2023): $139m in China

The franchise didn’t die, but it lost half its Chinese revenue just as production budgets were climbing toward $300m+

Jurassic World

Jurassic World (2015): $229m China

Fallen Kingdom (2018): $261m China

Dominion (2022): $158m China

A 40% decline in China box office between the second and third films in the trilogy, precisely when the franchise needed China most to justify another sequel

Remember the 3× rule? A film needs roughly 3× its production budget at global box office to break even after marketing and exhibitor splits.

For tentpole sequels budgeted at $200–300m, that means needing $600–900m globally. Pre-2020, you could reasonably model:

$250–350m domestic U.S.

$150–250m China

$250–400m rest-of-world

That formula is dead. Now you need:

$250–350m domestic U.S. (same)

$0–50m China (↓ 75–100%)

$400–550m rest-of-world (↑ 60–120%)

The problem? Rest-of-world doesn’t scale linearly. You can’t just add $200m to your European and Latin American take because China disappeared. Those markets have ceiling effects—smaller populations, lower ticket prices, more piracy.

And it’s not like American cultural soft power is growing internationally at the moment.

That’s all for this week; I hope you enjoyed it.

Cheers,

Wyatt

Disclosures & Disclaimers The information contained in this newsletter is provided for general informational purposes only and does not constitute investment, legal, tax, or other professional advice. Altea does not offer or sell securities through this newsletter. Any references to investment opportunities are not offers to buy or sell any security. You should not construe any such references as a recommendation to invest.

All investments carry risk and may result in loss. You are solely responsible for conducting your own due diligence and consulting with your own legal, tax, and investment advisors before making any investment decisions.

Altea does not guarantee the accuracy or completeness of information provided by third parties. Past performance is not indicative of future results.

Only accredited investors, as defined by applicable laws, may participate in Altea investment opportunities.